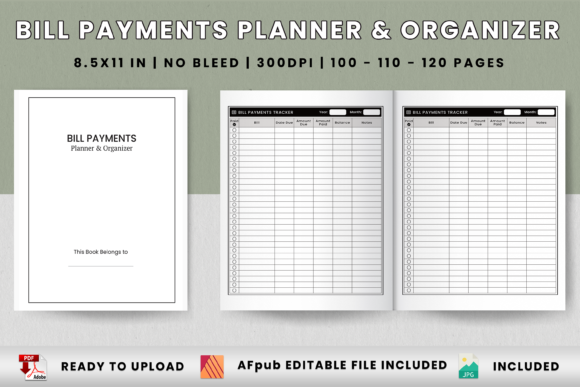

Evaluating the Monthly Bill Payment Planner Organizer for Personal Finance Management

Managing personal finances often requires a bridge between digital convenience and tangible accountability. For adults navigating complex billing cycles, subscription services, and variable expenses, the Monthly Bill Payment Planner Organizer serves as a dedicated analog interface for financial tracking. Unlike generic notebooks or automated banking apps, this specific tool is structured to provide a visual and tactile record of obligations. When considering resources for bill management, it is essential to understand how a dedicated planner compares to digital alternatives and general-purpose stationery, particularly regarding layout specificity, retention, and long-term utility.

Distinguishing Dedicated Planners from Generic Notebooks

A common point of comparison for individuals seeking better organization is the choice between a specialized Monthly Bill Payments Tracker and a standard blank or lined notebook. While a generic notebook offers maximum flexibility, it lacks the pre-structured cognitive scaffolding necessary for consistent financial tracking. A dedicated planner eliminates the setup friction that often leads to abandoned tracking habits.

The primary distinction lies in the pre-formatted architecture. A quality bill payment organizer typically includes specific columns for due dates, payee names, amounts owed, amounts paid, and confirmation numbers. In contrast, creating these tables manually in a blank notebook consumes time and mental energy every month. Furthermore, specialized trackers often integrate annual overviews and recurring expense logs that generic notebooks cannot replicate without significant user effort. For users who value immediate usability over creative freedom, the dedicated format provides a standardized system that reduces decision fatigue during monthly reviews.

Analog Tracking Versus Digital Automation

Digital tools and banking apps excel at automation and real-time data synchronization. However, they often fail to provide the holistic perspective needed for proactive budgeting. The Monthly Bill Payment Planner Organizer occupies a distinct niche by focusing on intentionality rather than mere transaction recording. Research into financial behavior suggests that the physical act of writing down payments can increase awareness of spending patterns and improve memory retention regarding financial obligations.

Digital solutions are superior for automatic alerts and historical data searching. Yet, they can create a passive relationship with money where bills are paid invisibly, potentially masking cash flow issues until an overdraft occurs. An analog tracker forces a monthly reconciliation ritual. This manual verification process acts as a safeguard against subscription creep and billing errors that automated systems might overlook. The tradeoff is clear: digital tools offer speed and integration, while the physical planner offers mindfulness and comprehensive oversight. Many financially savvy adults find that using both—a digital system for execution and a physical planner for strategy—provides the most robust defense against financial disorganization.

Technical Specifications and Production Quality

When evaluating printable or KDP-ready bill trackers, technical specifications directly impact the user experience. Not all PDF templates are created equal, and understanding production standards helps distinguish professional-grade resources from amateur designs.

- Dimensions: The 8.5x11 inch format is the industry standard for home printing and Amazon KDP. This size provides ample horizontal space for wide tracking tables, which is critical when documenting multiple data points per bill. Smaller formats like A5 or 6x9 inches may feel portable but often result in cramped writing areas that discourage detailed note-taking.

- Resolution: A minimum of 300 DPI (dots per inch) is non-negotiable for crisp text and clean lines. Low-resolution files appear pixelated when printed, making them difficult to read and unprofessional if bound. High-quality source files ensure that grid lines remain sharp and text remains legible even after repeated handling.

- Bleed Settings: For home printing or standard KDP paperback publishing, "no bleed" settings are generally preferable for functional planners. Bleed extends artwork to the edge of the paper, which risks cutting off important writing space near the margins during the trimming process. No-bleed designs maintain a safe margin, ensuring all tracking fields remain fully accessible and writable.

- Page Count Variations: Options ranging from 100 to 120 pages accommodate different tracking durations. A 100-page book may suffice for simple monthly tracking, while 120-page versions often include additional sections for annual summaries, debt payoff trackers, or savings goals. Evaluating your need for auxiliary pages versus pure bill tracking helps determine the optimal length.

Editability and Customization Potential

For creators or users with specific needs, the availability of editable source files, such as AFpub (Affinity Publisher), adds significant value beyond a static PDF. While a ready-to-print PDF is sufficient for immediate use, an editable source file transforms the product into a customizable platform.

Users with unique billing cycles, such as bi-weekly pay schedules or quarterly tax payments, may find standard layouts inadequate. Access to the source file allows for the modification of column headers, adjustment of row heights, or addition of custom categories. For those intending to publish their own branded version on Amazon KDP, the inclusion of bonus JPG files and editable masters streamlines the cover design and interior formatting process. This flexibility distinguishes premium resources from rigid, one-size-fits-all templates. However, this feature is only relevant for users comfortable with design software; for the average consumer, a well-designed static PDF remains the most practical choice.

Assessing Fit: When to Choose This Format

The Monthly Bill Payment Planner Organizer is not a universal solution. It is best suited for specific user profiles and financial situations. Understanding these fit parameters prevents frustration and ensures the tool aligns with actual needs.

Ideal Use Cases:

- Visual Learners: Individuals who struggle to grasp their financial picture through screens alone benefit from the spatial arrangement of a physical page.

- Variable Income Earners: Freelancers and gig workers whose income fluctuates require a flexible tracking system that doesn't rely on fixed automated transfers.

- Debt Reduction Focus: Those actively paying down debt often need to track extra payments and progress visually, which is more satisfying on paper than in a spreadsheet.

- Digital Detox Seekers: Users attempting to reduce screen time appreciate keeping financial administration separate from email and social media distractions.

Limitations and Alternatives:

If you require real-time balance updates, automatic categorization, or integration with investment accounts, a dedicated app or accounting software is superior. Similarly, if you travel frequently and cannot carry a physical book, cloud-based spreadsheets or mobile-friendly trackers offer necessary portability. The analog planner is a complementary tool for oversight and planning, not a replacement for secure digital banking infrastructure.

Making an Informed Selection

Selecting the right Monthly Bill Payments Tracker involves balancing structure with flexibility. When comparing options, examine sample pages to verify that the writing space accommodates your handwriting size and that the layout matches your billing frequency. Check whether the page count supports your intended duration of use; buying a new book every three months may be less economical than investing in a comprehensive annual system.

Consider the longevity of the format. A timeless, undated design allows you to start at any time and pause without wasting pages, whereas dated planners offer the convenience of pre-filled calendars at the cost of flexibility. Evaluate the inclusion of supplementary resources like bonus JPGs or source files based on your technical capability and long-term goals. Ultimately, the most effective organizer is one that reduces friction in your financial routine. Whether you choose a downloadable PDF for instant access or a professionally bound edition, the goal remains consistent: transforming bill payment from a source of anxiety into a manageable, documented process.

By carefully weighing the tactile benefits of analog tracking against the efficiency of digital tools, and by scrutinizing technical specifications like resolution and dimensions, adults can select a resource that genuinely enhances their financial literacy. The Monthly Bill Payment Planner Organizer represents a deliberate choice to engage more deeply with personal economics, providing a stable foundation upon which broader financial health can be built.